{kind=link}

Why speed matters for the person on the pavement

The moment a driver in Mexico City needs funds, seconds can change decisions—fuel, routes, food. DiDi Finance has aimed to reduce that gap between an incoming SPEI transfer and the usable balance on a card, and that focus shows up for real users today. For riders and drivers exploring quick cash options, didi prestamos is often the first link in the chain; improving approval time and disbursement directly changes daily choices and income reliability.

Where delays happen and what users actually notice

Processing latency typically crops up in three places: identity verification (KYC), interbank settlement (SPEI), and the authorization pipeline that posts money to a wallet or card. For a user, these technical stages are visible only as waiting—failed trips, cold engines, missed fares. DiDi Finance’s user-centered work reduces handoffs between these stages and trims redundant checks that don’t add risk but do add minutes.

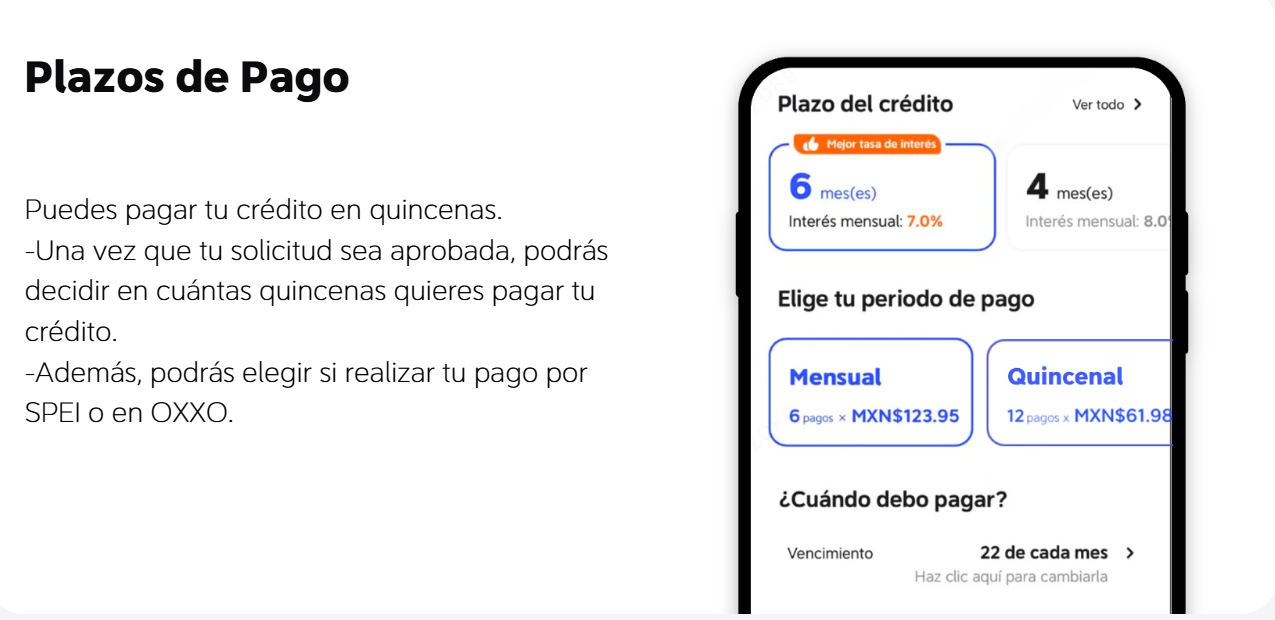

How DiDi Finance reorganizes the flow—practical moves

At the product level they prioritize steps that remove friction for recurring, low-risk transactions. That often means: faster KYC revalidation for returning users, parallelizing the authorization handshake with the issuing bank, and optimizing retry logic so temporary network blips don’t stall the whole process. These are concrete engineering trade-offs—faster authorization windows, reduced time-to-credit, and a smarter retry budget—that translate to usable balance arriving sooner.

User stories and a real-world anchor

During the 2020 pandemic surge in digital payments, drivers in urban centers like Mexico City reported longer settlement times as systems coped with volume spikes. Seeing that, product teams shifted focus from feature bloat to throughput—less glamour, more reliability. One driver’s note: faster releases meant taking a night shift without worry. That’s the kind of human metric DiDi Finance measures alongside technical KPIs.

Comparative insights: alternatives and trade-offs

Not every provider balances speed and risk the same way. Some platforms favor instant credit at higher underwriting cost; others prefer delayed clearing with lower fees. The right choice depends on the user’s tolerance for fees versus the need for immediate liquidity. For customers evaluating lending and release options, consider how providers handle authorization retries, fraud scoring thresholds, and settlement windows. For users also considering short-term lending, checking offerings like didi prestamos and didi credito (lending paths within the same ecosystem) clarifies whether speed comes bundled with costly credit or with smarter disbursement flows.

Common mistakes users and teams make

A frequent mistake is treating speed as a vanity metric—faster is only better if it’s reliable. Teams often rush feature launches to reduce latency without adequate monitoring; that creates intermittent failures that feel worse than a slow but steady service. Users often accept high fees for perceived speed without checking settlement transparency—an avoidable cost when providers clearly show authorization and settlement logs.

Three golden rules to evaluate instant-release and processing services

1) Measurement: prioritize providers that publish mean and tail latency for authorization and disbursement. Those numbers show real-world performance, not slogans.

2) Transparency: choose platforms that explain when they use credit lines versus true settlement. Knowing whether speed is funded by a short-term loan matters for cost and long-term planning.

3) Resilience: confirm the provider has retry logic, clear user-facing states, and fallbacks for failed SPEI settlements—this reduces user disruption and restores trust quickly.

Closing: practical value and next steps

Speed is a tool, not a promise. When implemented with clear metrics, sensible underwriting, and user-first fallbacks, faster card release means predictable income and smoother days for drivers and merchants alike. —Trust practical design over hype; the result is measurable: less downtime, fewer support tickets, and improved daily cash flow. DiDi Finanzas.