{kind=link}

Comparative lead: why this matters now

Many urban commuters in Mexico City and beyond turned to quick credit after the 2020 slowdown, so comparing options matters more than ever. This piece takes a side-by-side look at DiDi’s loan product through the lens of users and features — starting with didi finanzas as the focal service — and measures it against common online lenders on speed, fees, and trust signals.

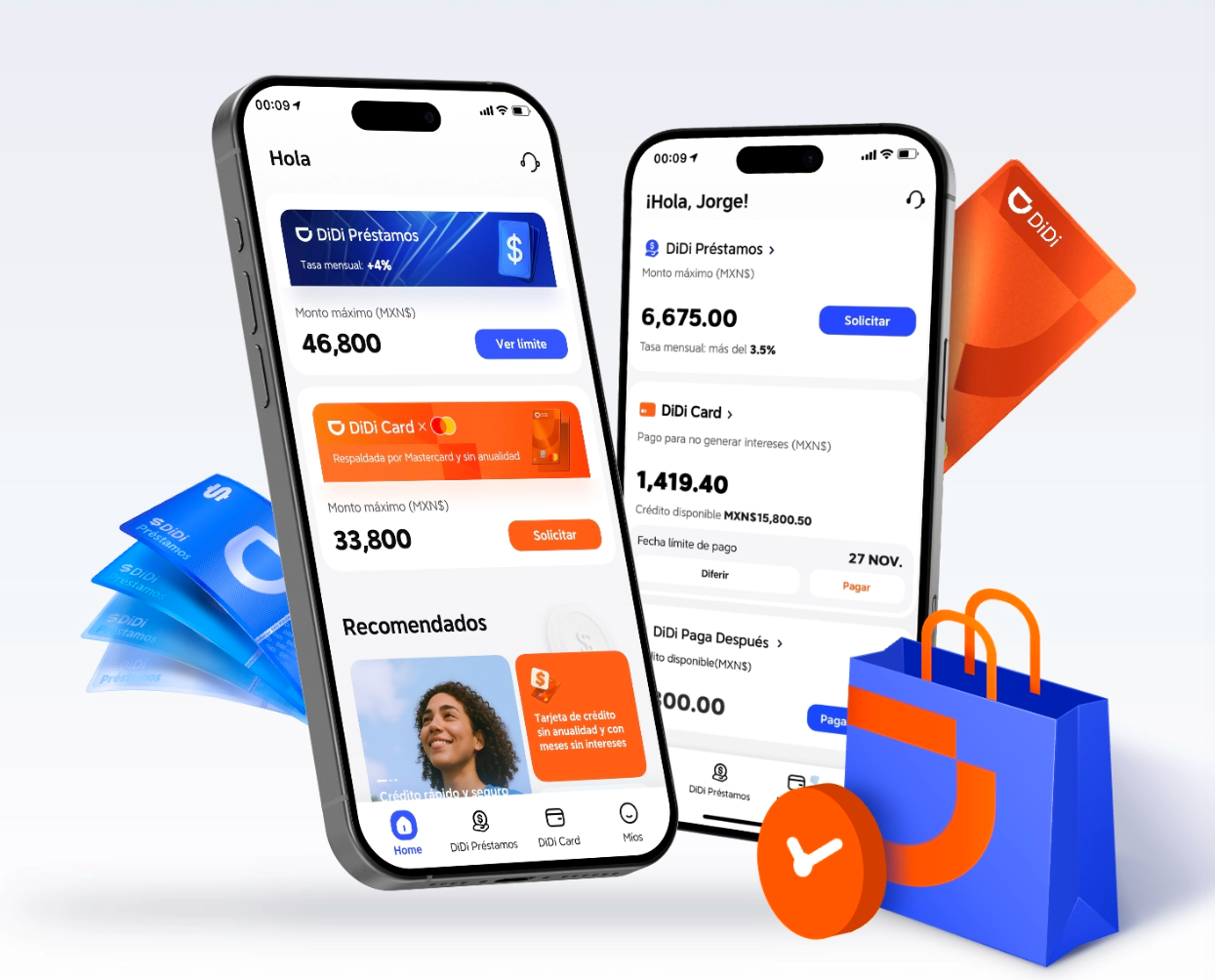

How DiDi loans operate: core mechanics

DiDi’s lending process is built into a mobile app and follows familiar steps: KYC verification, soft credit checks to assess credit score, and automated underwriting to set limits. The experience is typically app-driven, with disbursement into a digital wallet or bank account. Expect standard industry terms like APR and repayment schedule to be displayed during checkout; transparency varies by lender but is central to a fair contract.

Direct comparison: fees, speed, and customer experience

Here is a practical contrast between DiDi loans and typical online lending apps.

– Speed: DiDi often promises same-day decisions thanks to automated underwriting; many competitors match this, though transfer speeds depend on the receiving bank.

– Fees and APR: DiDi’s fee structure tends to be competitive for small, short-term amounts, but effective APR can rise with late fees — read the repayment table. Other apps may appear cheaper upfront yet add processing or origination fees that change the landed APR.

– UX and support: DiDi’s interface is straightforward for drivers and riders familiar with the main app. Alternatives focused solely on credit sometimes offer more detailed customer service channels and clearer dispute mechanisms.

Common mistakes applicants make include accepting the first offer without checking total cost, and skipping documentation that would improve loan limits — both affect underwriting outcomes and long-term costs.

Real user feedback and trust signals

Users report mixed experiences: many praise fast approvals and intuitive app flows, while a minority note opaque penalty terms or slower transfers to some banks. Trust signals to check: licensing statements in app stores, customer reviews on independent platforms, and whether the app displays its regulatory jurisdiction. For a direct look at company transparency, see didi finanzas es confiable.

When DiDi loans make sense — and when to pause

DiDi loans fit short-term cash needs tied to platform income cycles, such as covering vehicle costs between payouts. They are sensible when you can repay within one billing cycle and want a quick, app-integrated solution. Avoid them for long-term financing or recurring gaps in income — that pattern raises you into higher APR territory and risks repeated fees. — Think of small, planned uses rather than habitual bridging.

Alternatives and typical pitfalls

Alternatives include peer-to-peer lenders, credit cards (if you can access low-interest offers), and employer-linked advances. Pitfalls common across providers are unclear origination fees, aggressive collections, and repeated soft-to-hard credit transitions that can affect credit score. Always compare total repayment, not only headline rates.

Three golden rules for choosing a short-term loan

1) Measure total cost: confirm the full APR and all fees before accepting. Use installment breakdowns to see real monthly impact.

2) Verify repayment fit: ensure the payment schedule aligns with expected inflows; avoid loans that require repayments before your next confirmed income.

3) Check trust markers: licensing, clear KYC flow, and accessible dispute channels matter as much as speed. Prefer lenders that show transparent underwriting criteria.

Applied correctly, these rules reduce surprises and protect your earning rhythm—DiDi’s app integration can be convenient for platform workers when those conditions line up. DiDi Finanzas — practical, not perfect.